what is a deferred tax provision

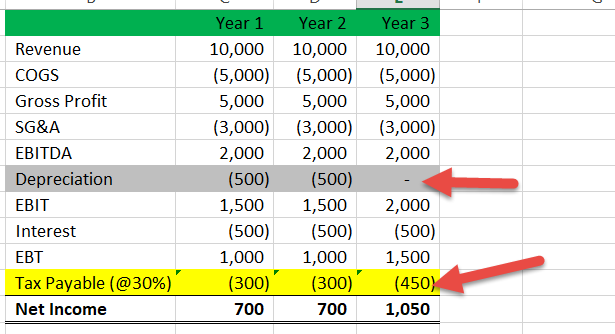

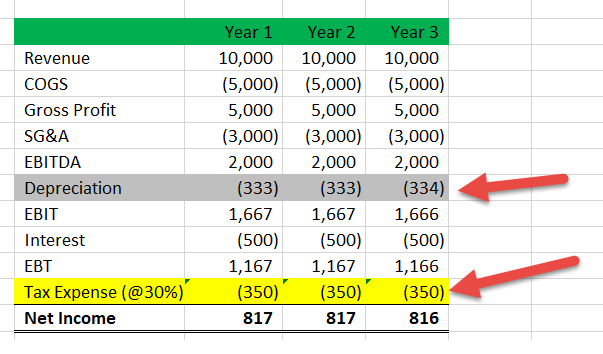

Now see that if deferred tax is not recognized provision for taxation isfluctuating significantly each year and so is the profit after tax figure despite same profit before tax in each year. Deferred tax refers to either a positive asset or negative liability entry on a companys balance sheet regarding tax owed or overpaid due to temporary differences.

Deferred Tax Liabilities Meaning Example Causes And More

Deferred tax is the tax effect of timing differences.

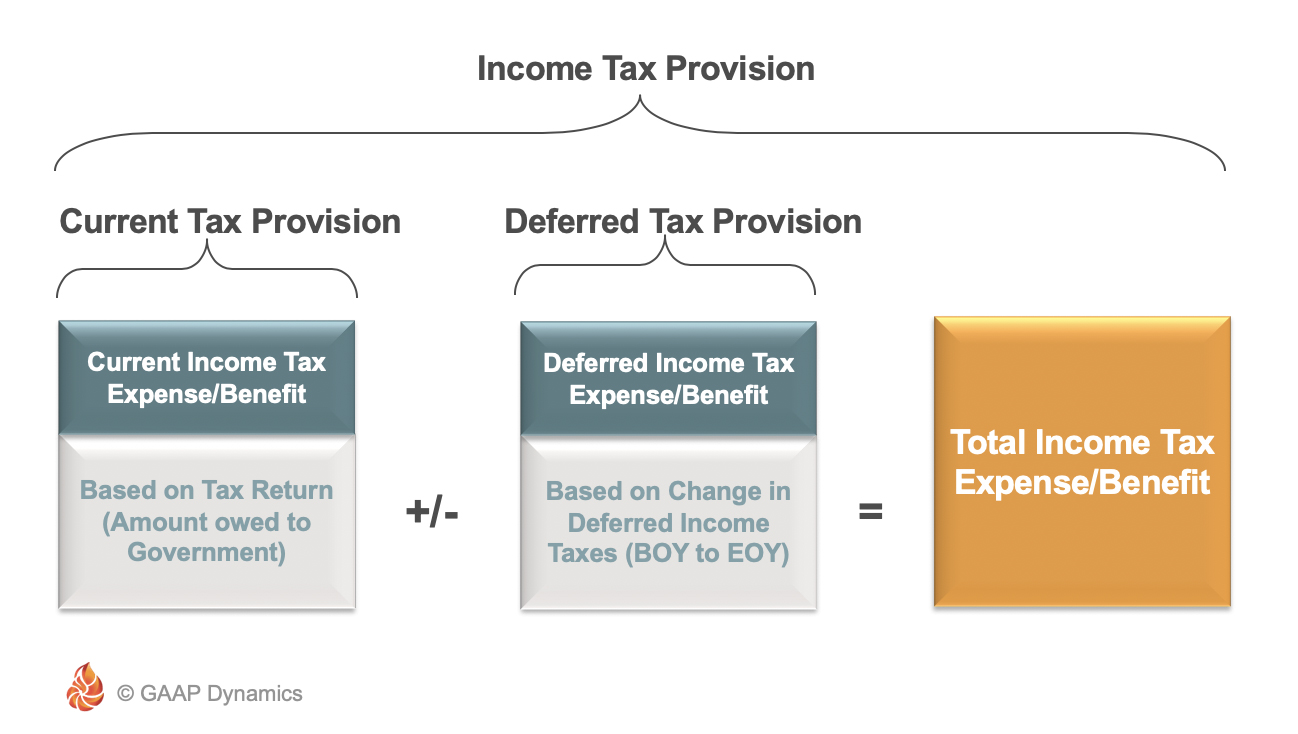

. The current tax provision is the amount chargeable to the financial result for the year while the deferred tax provision is the amount of tax that will be chargeable against the financial results of the business in future years. As per this definition there are two types of deferred tax-deferred tax asset and deferred tax liability. The fluctuation is only due to temporary timing.

Deferred income tax expense benefit represents the anticipated future tax expense benefit from activity in past or current periods. Watch out a lot more about it. On the contrary if a given liability has a carrying value lesser than the tax base in that case too a temporary difference.

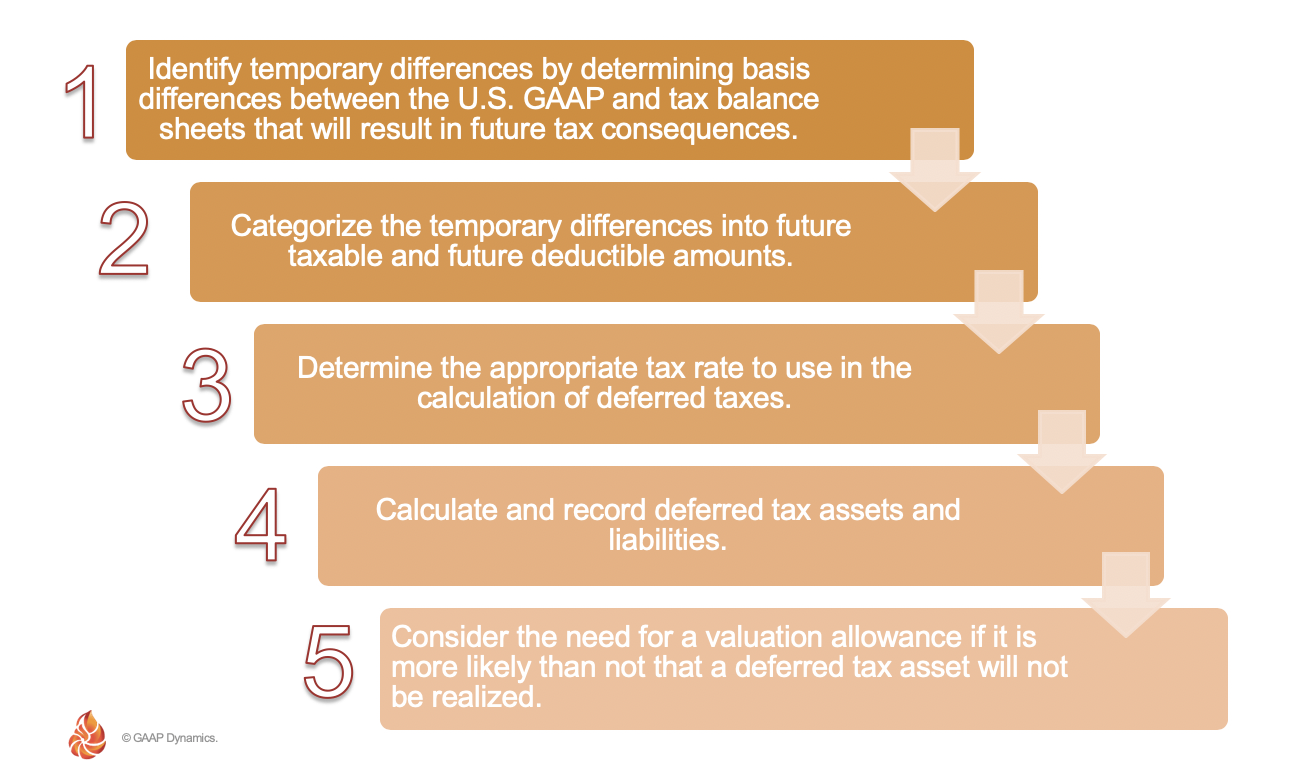

Companies first need to calculate their current income taxes payable or receivable then figure out their deferred tax assets and liabilities. What is deferred tax. Generally FRS 102 adopts a timing difference approach ie deferred tax is recognised when items of income and expenditure are.

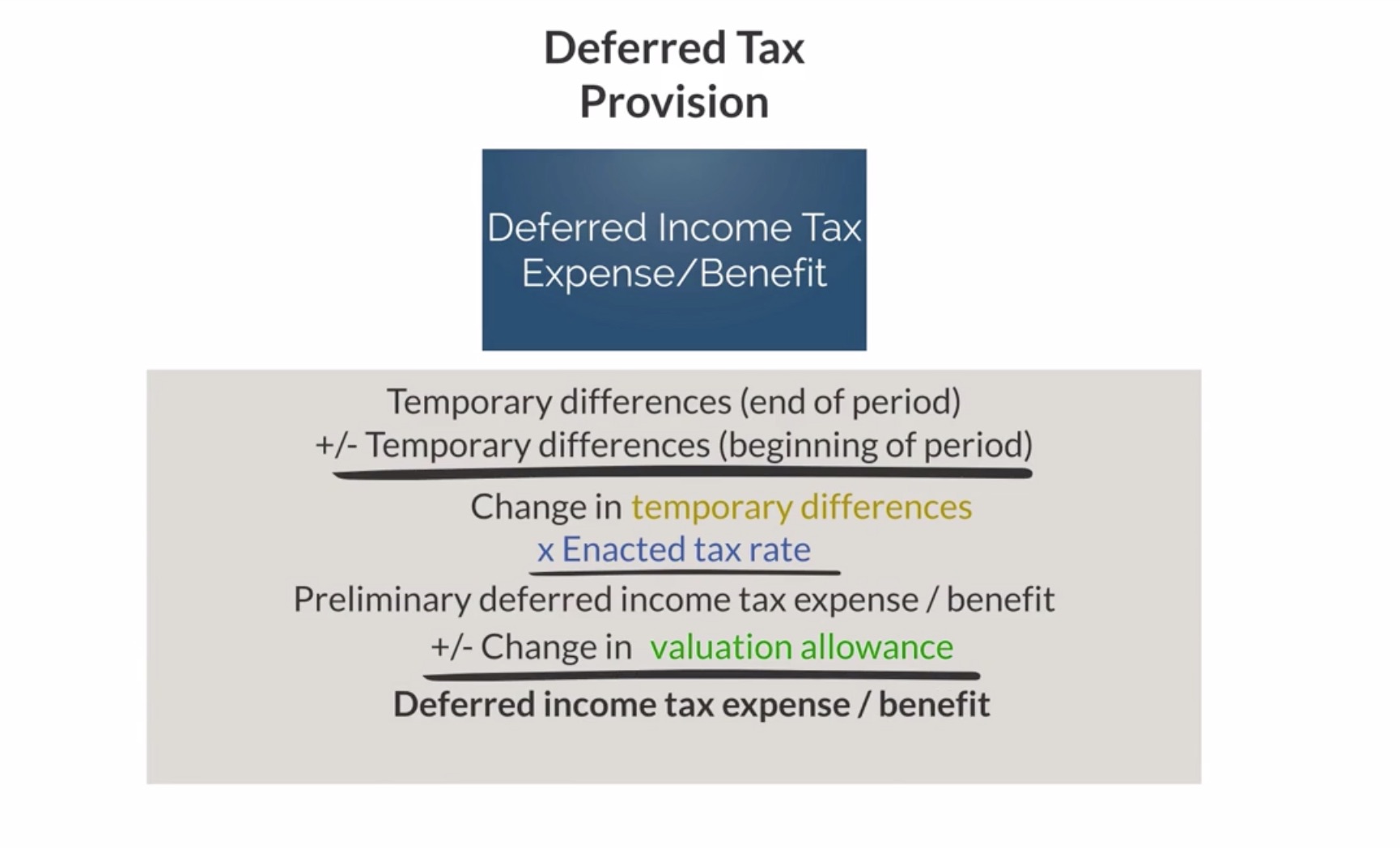

Around the world governments are stepping in to try and limit the impact of the pandemic by providing financial support in numerous ways from direct cash payments through to the deferral of tax payments. Deferred tax expense or benefit generally represents the change in the sum of the deferred tax assets net of any valuation allowance and deferred tax liabilities during the year. Try it free for 7 days.

This more complicated part of the income tax provision calculates a cumulative total of the temporary differences and applies the appropriate tax rate to that total. Deferred tax is a provision in your companys accounts which is required by FRS 102 and FRS 102 1A but not by FRS 105 the standard for micro entities and is used to accrue tax to the appropriate accounting periods. If deferred tax provision in not recognized then Profit and loss Account would look like as follows.

Putting through a deferred tax charge is a way of evening out these differences so that the company doesnt overestimate its profit. Keep track of your business tax with instant financial reports at your fingertips with Debitoor accounting invoicing software. These future expenses benefits arise due to temporary differences between book and tax value for certain items.

The deferred income tax is a liability that the company has on its balance sheet but that is not due for payment yet. Deferred tax is the amount of tax payable or recoverable in future reporting periods as a result of transactions or events recognised in current or previous periods accounts. Deferred income tax expense.

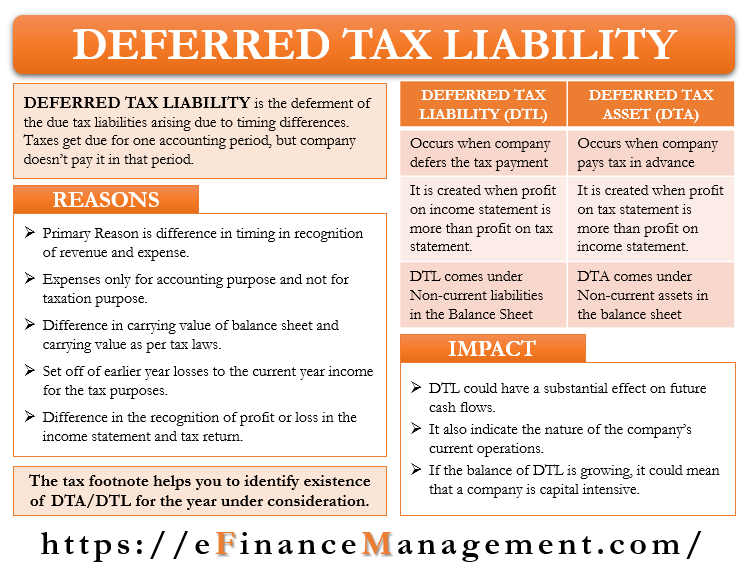

The company usually either has deferred tax liability or deferred tax asset as the deferred tax would be net off between deferred tax liability and deferred asset. A deferred tax asset is an asset to the Company that usually arises when either the Company has overpaid taxes or paid advance tax. Such taxes are recorded as an asset on the balance sheet and are eventually paid back to the Company or deducted from future taxes.

Deferred tax liability is created when the Company underpays the tax which it will have to pay in the near future. This article Deferred tax provisions 123 kb sets out four key areas of your tax provision that could be affected by the impacts of COVID-19. A company recognises deferred tax when recovering an asset or settling a liability in the future will have tax consequences that is will affect the amount of tax the company will pay.

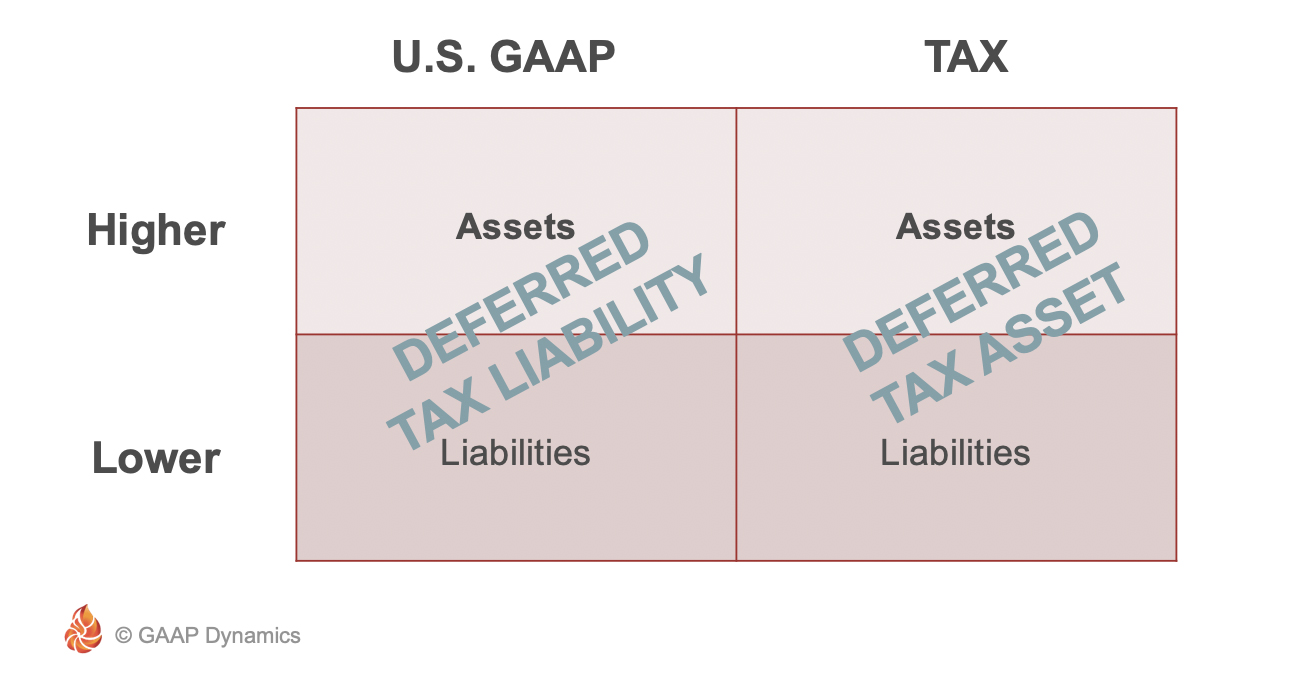

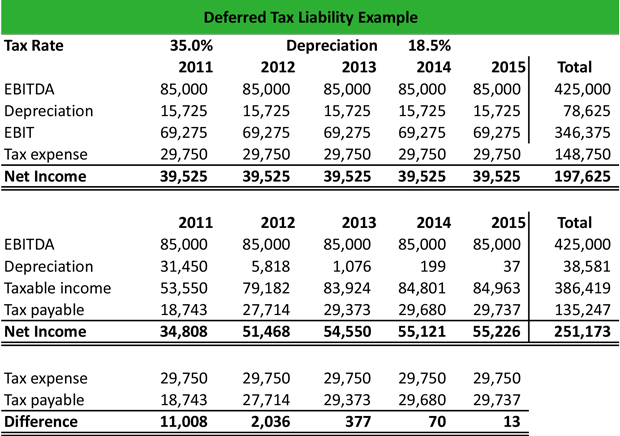

Deferred tax charge is not a provision for tax but is a provision for tax effect for difference between taxable income and accounting income and further that deferred tax charge cannot be termed as income-tax paid or payable which has to be paid out of the profit earned. Deferred tax liability is created in the case where the carrying value of an asset is greater than the tax base. The liability is created not due to Company defaulting on its tax liabilities but due to timing mismatch or accounting provisions Accounting Provisions The provision in accounting refers to an amount or obligation set aside by the business for present and future commitments.

Deferred Tax means the deferment of taxes due to temporary differences. How do companies report deferred tax. Deferred tax is a topic that is consistently tested in Financial Reporting FR and is often tested in further detail in Strategic Business Reporting SBR.

DTA arises if you are required to pay more tax in future and DTL arises if you have paid more tax today and are thus required to pay less tax in the future. Both the current and deferred tax provis. ASC 740 applies to all entities but only to entity-level taxes.

Deferred income tax is a result of the difference in income recognition between tax laws ie the IRS and accounting methods ie GAAP. Timing differences are the differences between taxable income and accounting income for a period that originate in one period and are capable of reversal in one or more subsequent periods. The term deferred tax in essence refers to the tax which shall either be paid or has already been settled due to transient inconsistency between an organisations income statement and tax statement.

A provision is created when deferred tax is charged to the profit and loss account and this provision is reduced as the timing difference reduces. Deferred tax can fall into one of two categories. Deferred tax represents amounts of income tax payable or recoverable in the future.

A deferred tax liability is a listing on a companys balance sheet that records taxes that are owed but are not due to be paid until a. A deferred tax of any type is recorded in the balance sheet of an. This article will start by considering aspects of deferred tax that are relevant to FR before moving on to the more complicated situations that may be tested in SBR.

The tax may be required to be paid in future. Deferred tax is the tax effect that occurs due to the temporary differences either taxable temporary difference or deductible temporary difference. The provision has two components the current and deferred tax amounts.

Accounting For Income Taxes Under Asc 740 Deferred Taxes Gaap Dynamics

Define Deferred Tax Liability Or Asset Accounting Clarified

How Is A Deferred Tax Liability Or Asset Created Quora

Accounting For Income Taxes Under Asc 740 An Overview Gaap Dynamics

Deferred Tax Liabilities Meaning Example How To Calculate

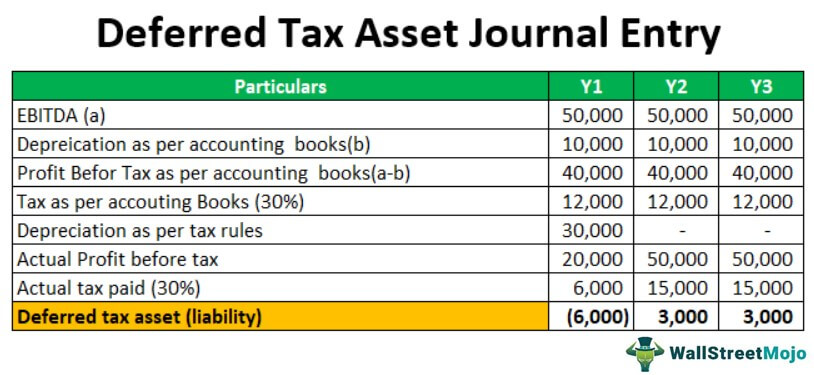

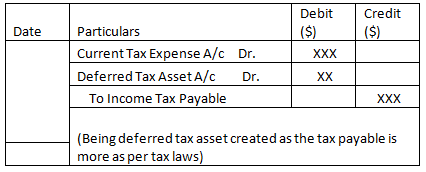

Deferred Tax Asset Journal Entry How To Recognize

Deferred Tax Double Entry Bookkeeping

Deferred Tax Liabilities Meaning Example How To Calculate

/dotdash_Final_Deferred_Tax_Asset_Definition_Aug_2020-01-dab264b336b94f939b132c55c018f125.jpg)

Deferred Tax Asset Definition

Computation Of Deferred Tax Liabilities

Worked Example Accounting For Deferred Tax Assets The Footnotes Analyst

/dotdash_Final_Deferred_Tax_Asset_Definition_Aug_2020-01-dab264b336b94f939b132c55c018f125.jpg)

Deferred Tax Asset Definition

What Is A Deferred Tax Liability Dtl Definition Meaning Example

Deferred Tax Asset Journal Entry How To Recognize

Accounting For Income Taxes Under Asc 740 Deferred Taxes Gaap Dynamics

Accounting For Income Taxes Under Asc 740 Deferred Taxes Gaap Dynamics

Deferred Tax Asset Deferred Tax Assets Vs Deferred Tax Liability

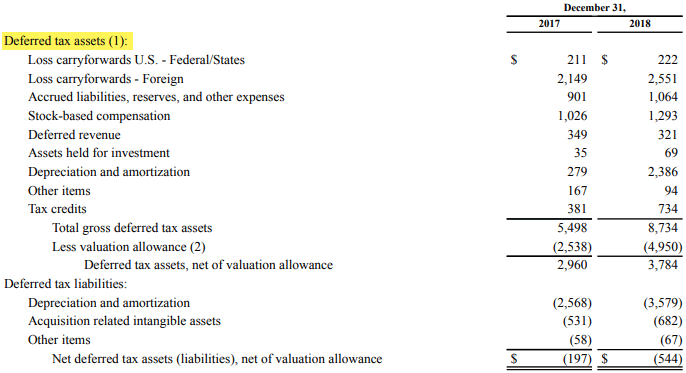

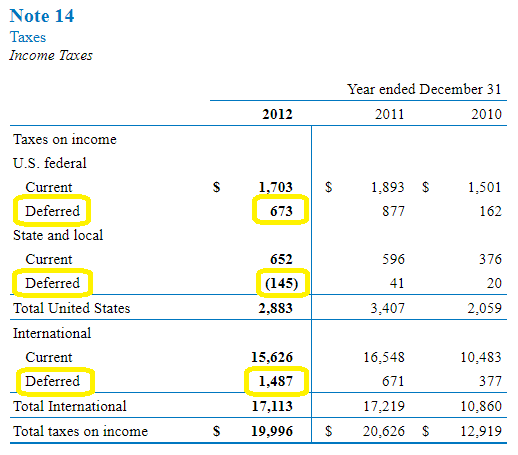

Deferred Income Tax Liabilities Explained With Real Life Example In A 10 K

:max_bytes(150000):strip_icc()/dotdash_Final_Deferred_Tax_Asset_Definition_Aug_2020-01-dab264b336b94f939b132c55c018f125.jpg)

Deferred Tax Asset Definition